Bitcoin Futures Demand Falls to Lowest Since 2024, but CME Open Interest Signals Resilience

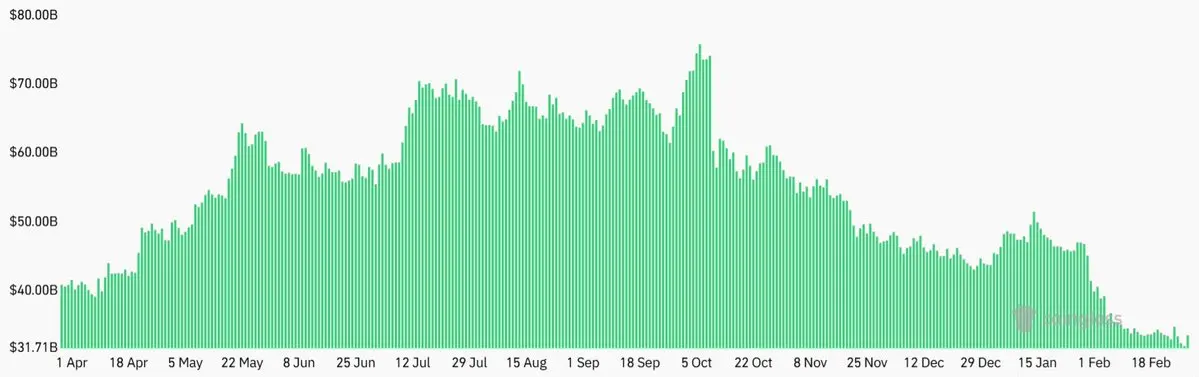

Bitcoin futures aggregate open interest on major exchanges declined to $32 billion on March 1, 2026, down 20% from one month prior, reaching its lowest level since August 2024 when measured in Bitcoin terms at 491,300 BTC.

Bitcoin futures aggregate open interest on major exchanges declined to $32 billion on March 1, 2026, down 20% from one month prior, reaching its lowest level since August 2024 when measured in Bitcoin terms at 491,300 BTC.

The annualized premium on monthly futures contracts dropped to 2%, the lowest in a year and below the neutral 5% to 10% range that typically compensates for longer settlement periods. Despite these indicators suggesting reduced demand for leveraged bullish positions, CME Bitcoin futures open interest remains elevated at $7.5 billion, and spot Bitcoin ETFs continue to trade over $3 billion in average daily volume, indicating institutional participation persists despite market hesitation.

Futures Demand Declines to Multi-Year Lows

Bitcoin’s price recovery to approximately $69,000 on March 2 followed a weekend low near $63,000, but futures market data reveals underlying caution among traders. Aggregate open interest across major cryptocurrency exchanges fell to $32 billion, representing a 20% decline over the preceding month. In Bitcoin-denominated terms, open interest reached 491,300 BTC, the lowest level since August 2024.

(Source: CoinGlass)

(Source: CoinGlass)

The decline partially reflects forced liquidations of bullish positions following Bitcoin’s 45% correction from its October 2025 all-time high of $126,200. Demand for leveraged long exposure has remained largely absent since that peak, with futures markets showing persistent weakness over the past 12 months.

The annualized premium, or basis rate, on Bitcoin monthly futures contracts dropped to 2%, its lowest level in a year. Under normal market conditions, this metric ranges from 5% to 10% to compensate traders for the longer settlement period. More concerning for bulls, the basis rate has failed to sustain levels above this neutral range for an entire year, a period that included a 50% rally between April and May 2025.

Options Market Shows Resilience Despite Bearish Sentiment

The Bitcoin options market provides a more nuanced picture of trader positioning. The put-to-call options premium at Deribit remained near 0.7 on March 2, indicating that demand for put (sell) options continues to trail demand for call (buy) options. A brief spike in bearish positioning on February 28 did not persist, suggesting options traders have not priced in sustained downside stress.

The put-to-call ratio measures the relative volume of bearish versus bullish options contracts. Readings below 1.0 indicate higher demand for calls, which profit from upward price movement, while readings above 1.0 suggest put demand dominates. The sustained sub-1.0 reading indicates that options traders have not capitulated despite Bitcoin’s extended downturn.

Institutional Participation Evidence Contradicts Exit Narratives

Despite declining futures demand, multiple indicators suggest institutional investors have not abandoned the Bitcoin market. Spot Bitcoin ETFs continue to trade over $3 billion in average daily volume, with holders including some of the world’s largest mutual and pension fund managers.

Onchain data shows publicly listed companies collectively hold over $79 billion in Bitcoin. Major corporate holders include Strategy, MARA Holdings, XXI, and Metaplanet. Several sovereign nations, including Bhutan, El Salvador, and the United Arab Emirates, have also added Bitcoin exposure to their reserves.

CME Bitcoin futures open interest stands at approximately $7.5 billion, representing institutional activity through regulated derivatives channels. This metric has remained relatively stable even as aggregate open interest across all exchanges declined, suggesting that institutional positioning differs from retail sentiment.

The derivatives market structure inherently requires balanced positioning, as every short order must be matched by a long order. The current environment reflects reduced appetite for leveraged long exposure rather than active institutional exit.

Market Context and Broader Trends

Bitcoin’s underperformance relative to gold and traditional equity markets has likely contributed to reduced attention from speculative traders. Gold has surged approximately 80% over the past year to record highs above $5,300, while Bitcoin remains 45% below its all-time peak.

The total cryptocurrency market capitalization stands at approximately $1.4 trillion, having demonstrated resilience through multiple geopolitical and macroeconomic shocks. Bitcoin’s fixed supply and network security continue to function as designed despite the extended price correction.

While it remains unclear whether the $60,000 level represents the cycle bottom, derivatives data suggests the market structure remains intact. The absence of sustained stress signals in options markets and persistent institutional presence through ETFs and CME futures indicate continued functionality of Bitcoin’s core market infrastructure.

FAQ: Bitcoin Futures Demand and Institutional Positioning

What does declining Bitcoin futures open interest indicate about market sentiment?

The 20% decline in aggregate open interest to $32 billion and the drop in Bitcoin-denominated open interest to 491,300 BTC (lowest since August 2024) indicates reduced demand for leveraged bullish positions. The annualized futures premium falling to 2%, well below the neutral 5-10% range, confirms that traders are hesitant to deploy leverage despite recent price recovery.

Are institutional investors exiting the Bitcoin market?

Available evidence suggests institutions have not exited. CME Bitcoin futures open interest remains elevated at $7.5 billion, spot Bitcoin ETFs trade over $3 billion daily, and publicly listed companies hold over $79 billion in Bitcoin onchain. Sovereign nations including Bhutan, El Salvador, and the UAE have also added Bitcoin exposure. The decline in futures demand reflects reduced leverage appetite rather than institutional capitulation.

How has Bitcoin’s options market reacted to the recent price volatility?

The Bitcoin put-to-call options premium has remained near 0.7, indicating higher demand for call options than puts. A brief spike in bearish positioning on February 28 did not persist, and the options market shows no signs of major stress or sustained derivatives dysfunction despite Bitcoin trading 45% below its all-time high.

Related Articles

Data: In the past 24 hours, the entire network has been liquidated for $399 million, mainly long positions.

Trump Brothers' American Bitcoin Boosts Mining Capacity Following Q4 Loss

Glassnode: The selling pressure of long-term BTC holders is weakening