The Blockchain Revolution is Underway; Ethereum Remains Bullish.

After the market crash on October 11, the crypto market remained sluggish, with both market makers and investors suffering significant losses. Recovery of capital and sentiment will require time. Still, volatility and new opportunities are always present in crypto, so we remain optimistic about the future. The trend of mainstream crypto assets integrating with traditional finance to create new business models continues, and in fact, this integration accelerates and strengthens competitive advantages during market downturns.

I. Wall Street Consensus Grows Stronger

On December 3, U.S. SEC Chairman Paul Atkins said in an exclusive FOX interview at the New York Stock Exchange, “In the next few years, the entire U.S. financial market could move onto the blockchain.”

Atkins noted:

(1) The core benefit of tokenization is that, when assets are on-chain, both ownership structure and asset attributes become highly transparent. Today, public companies often lack clear knowledge of exactly who their shareholders are, where they are, or where their shares are held.

(2) Tokenization could also enable “T+0” settlement, replacing the current “T+1” trading settlement cycle. In principle, on-chain delivery versus payment (DVP) and receive versus payment (RVP) mechanisms can reduce market risk and enhance transparency. The current lag between clearing, settlement, and fund delivery is a major source of systemic risk.

(3) He believes tokenization is the inevitable direction for financial services, and major banks and brokerages are already moving in that direction. This could become reality worldwide in less than 10 years—perhaps within just a few years. We are actively adopting new technologies to ensure the U.S. remains at the forefront of cryptocurrency and related fields.

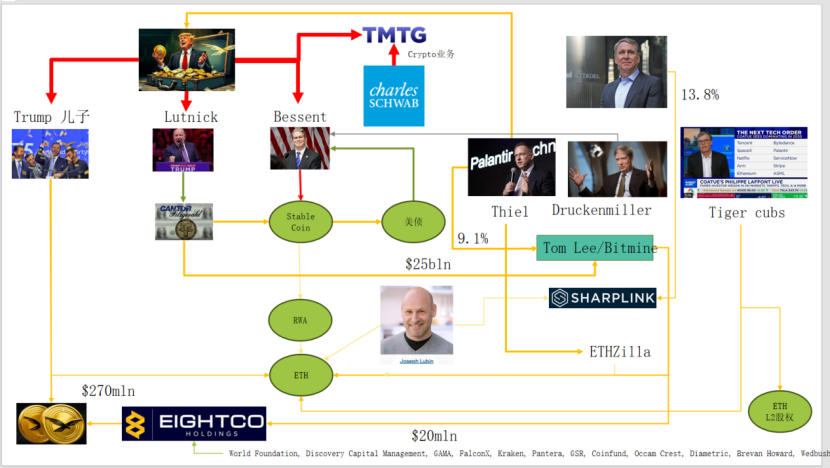

In practice, Wall Street and Washington have already built a deep crypto capital network, forming a new narrative chain: U.S. political and business elites → U.S. Treasuries → stablecoin/crypto custody firms → Ethereum + RWA + L2.

This graphic shows how the Trump family, traditional bond market makers, the Treasury Department, tech companies, and crypto firms are intricately connected, with the green elliptical lines forming the main backbone:

(1) Stablecoins (USDT, USDC, U.S. dollar assets backing WLD, etc.)

Major reserve assets are short-term U.S. Treasuries and bank deposits, held via brokerages like Cantor.

(2) U.S. Treasuries

Issued and managed by the Treasury/Bessent

Used by Palantir, Druckenmiller, Tiger Cubs, and others as low-risk, yield-generating base assets

Also the yield assets targeted by stablecoin/treasury management companies.

(3) RWA

From U.S. Treasuries, mortgages, and receivables to housing finance

Tokenized through Ethereum L1/L2 protocols.

(4) ETH & ETH L2 Equity

Ethereum serves as the main chain for RWA, stablecoins, DeFi, and AI-DeFi

L2 equity/tokens represent claims on future trading volume and transaction fee cash flows.

This chain illustrates:

U.S. dollar credit → U.S. Treasuries → stablecoin reserves → various crypto treasuries/RWA protocols → ultimately settling on ETH/L2.

In terms of RWA TVL, compared to other public chains that declined after October 11, ETH is the only one to quickly recover and rise. Its current TVL is $1.24 billion, accounting for 64.5% of the total crypto market.

II. Ethereum’s Value Capture Advancements

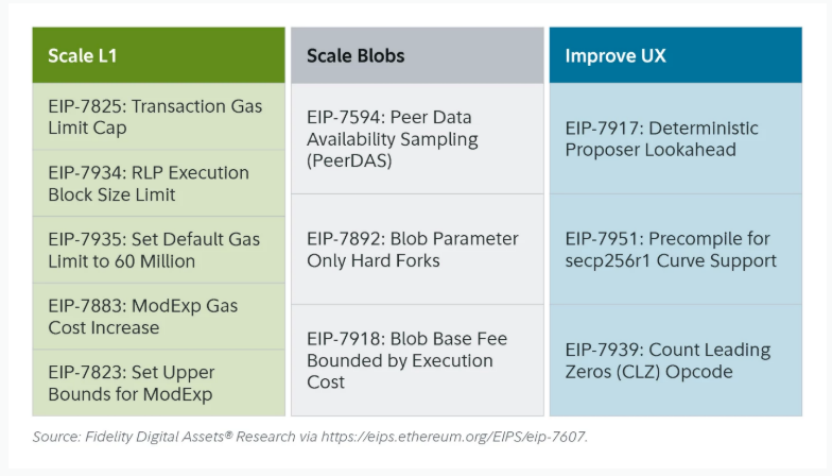

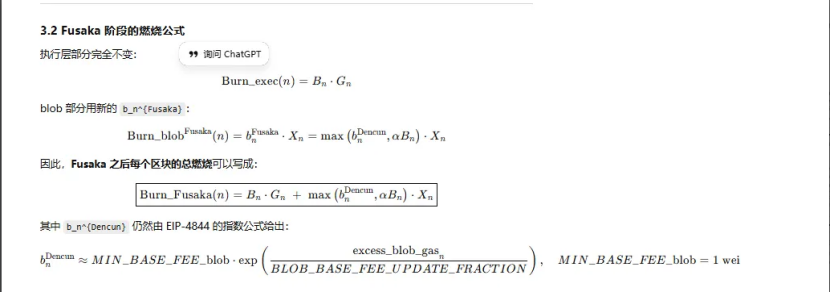

Ethereum’s recent Fusaka upgrade did not cause much market stir, but from the perspective of network structure and economic model evolution, it is a milestone. Fusaka goes beyond scaling via EIPs like PeerDAS; it aims to address the L1 mainnet’s insufficient value capture since the rise of L2.

With EIP-7918, ETH introduces the blob base fee as a “dynamic floor price,” pegging its lower bound to the L1 execution layer base fee. Blobs must pay DA fees at a unit price of roughly 1/16 the L1 base fee. This means rollups can no longer occupy blob bandwidth at near-zero cost for extended periods. These fees are burned and flow back to ETH holders.

There have been three Ethereum upgrades related to “burning”:

(1) London (single dimension): burns the execution layer; ETH began structural burning based on L1 usage

(2) Dencun (dual dimension + independent blob market): burns execution layer and blob; L2 data written to blobs also burns ETH, but in low demand, the blob portion is nearly zero.

(3) Fusaka (dual dimension + blob bound to L1): using L2 (blob) requires paying and burning at least a fixed proportion of the L1 base fee, so L2 activity is more stably mapped to ETH burning.

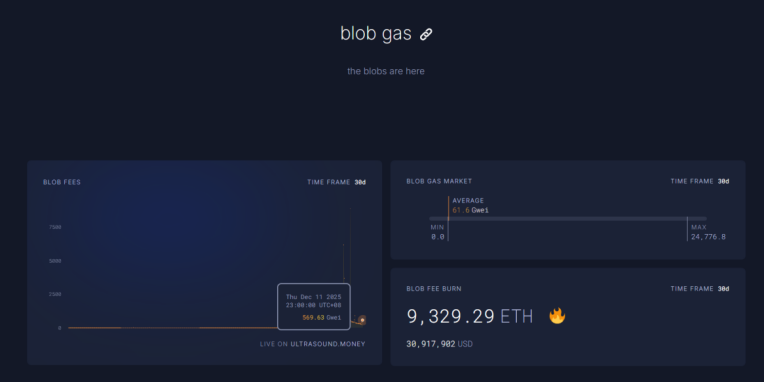

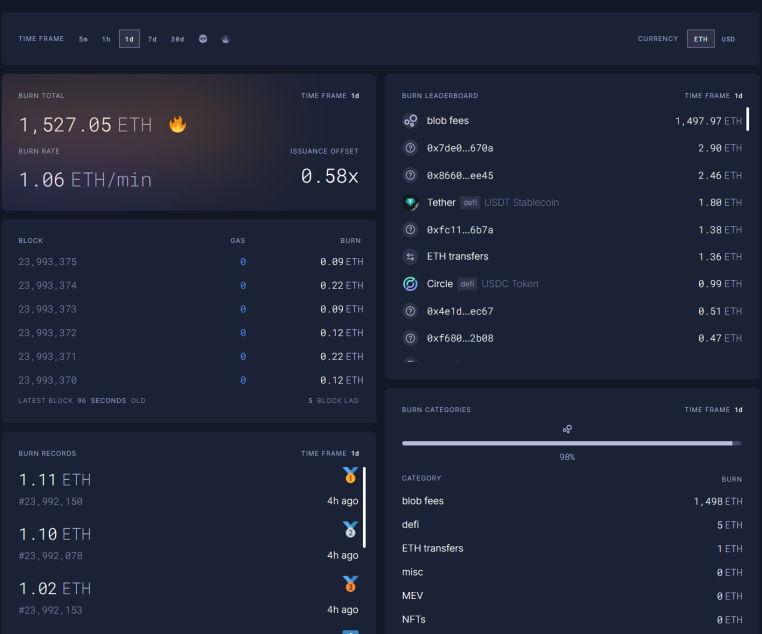

Currently, blob fees for the one-hour period at 23:00 on December 11 have surged to 569.63 billion times their pre-Fusaka upgrade level, with 1,527 ETH burned in a single day. Blob fees now account for 98% of burned ETH—the highest share ever. As ETH L2 activity increases, this upgrade could return ETH to a deflationary state.

III. Ethereum Technicals Show Strength

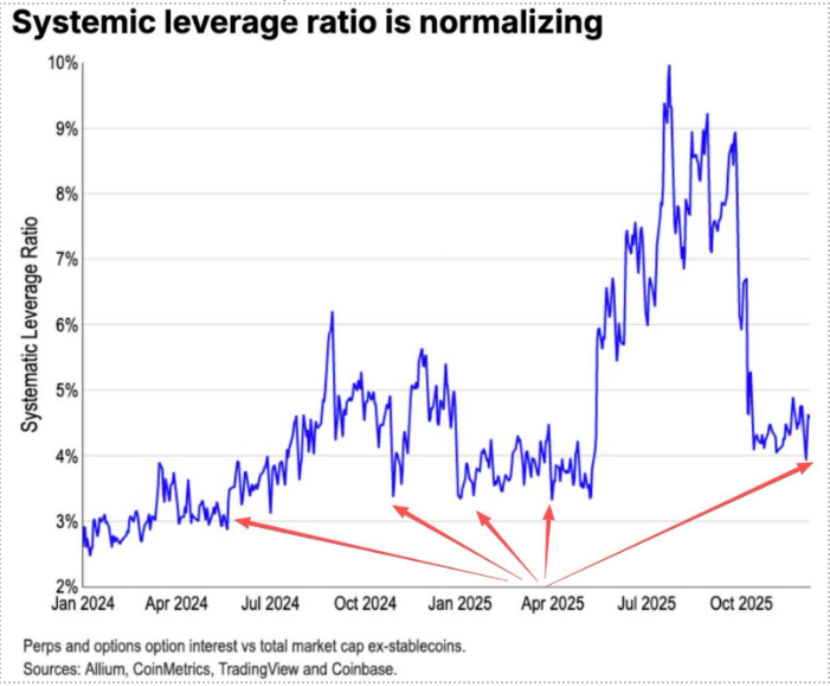

During the October 11 correction, leveraged ETH futures positions were fully liquidated, eventually triggering spot leveraged positions. Many lacking conviction in ETH—including numerous long-time OGs—reduced their holdings and exited. According to Coinbase, speculative leverage in crypto has dropped to a historic low of 4%.

Historically, a key source of ETH shorts was the Long BTC/Short ETH pair trade, which typically performed well in bear markets. This time, however, the outcome was different. The ETH/BTC ratio has remained flat since November.

Currently, 13 million ETH—about 10% of total supply—remain on exchanges, a historic low. As the Long BTC/Short ETH trade has failed since November, extreme market panic could gradually create a “short squeeze” opportunity.

As we approach 2025–2026, both U.S. and Chinese monetary and fiscal policy signals have turned friendly:

The U.S. will take proactive steps, cutting taxes, lowering rates, and easing crypto regulations. China will maintain moderate easing and financial stability, suppressing volatility.

With expectations of relative easing in both China and the U.S., and suppressed downside volatility in assets, while panic persists and capital and sentiment have yet to fully recover, ETH remains in a favorable “strike zone” for buying.

Statement:

- This article is republished from [[](https://trendresearch.medium.com/%E5%8C%BA%E5%9D%97%E9%93%BE%E9%9D%A9%E5%91%BD-%E8%BF%9B%E8%A1%8C%E6%97%B6-%E6%8C%81%E7%BB%AD%E7%9C%8B%E6%B6%A8%E4%BB%A5%E5%A4%AA%E5%9D%8A-7ffb991b0cb1)[Trend Research](https://trendresearch.medium.com/?source=post_page---byline--7ffb991b0cb1---------------------------------------)\], with copyright belonging to the original author [Trend Research]. If you have any objections to this republication, please contact the Gate Learn team, and we will address it promptly according to our procedures.

- Disclaimer: The views and opinions expressed in this article are solely those of the author and do not constitute investment advice.

- Other language versions of this article are translated by the Gate Learn team. Without specific reference to Gate, it is prohibited to copy, distribute, or plagiarize the translated article.

Share

Content

Related Articles

What Is Ethereum 2.0? Understanding The Merge

Reflections on Ethereum Governance Following the 3074 Saga

Our Across Thesis

What is Neiro? All You Need to Know About NEIROETH in 2025

An Introduction to ERC-20 Tokens