Futures

Hundreds of contracts settled in USDT or BTC

TradFi

Gold

One platform for global traditional assets

Options

Hot

Trade European-style vanilla options

Unified Account

Maximize your capital efficiency

Demo Trading

Futures Kickoff

Get prepared for your futures trading

Futures Events

Join events to earn rewards

Demo Trading

Use virtual funds to experience risk-free trading

Launch

CandyDrop

Collect candies to earn airdrops

Launchpool

Quick staking, earn potential new tokens

HODLer Airdrop

Hold GT and get massive airdrops for free

Launchpad

Be early to the next big token project

Alpha Points

Trade on-chain assets and earn airdrops

Futures Points

Earn futures points and claim airdrop rewards

Quantum Computing 2026: IBM Clarifies Superconducting Path, Two Sessions Call for Strong Promotion

In February 2026, IBM explicitly clarified its quantum computing timeline during the Barclays “Quantum Unlock 1.0” investor event—aiming to achieve “quantum advantage” by 2026 and fault-tolerant computing by 2029. This roadmap offers the most actionable technical milestones to date, marking the transition of quantum computing from laboratory validation to industrial deployment.

How can we understand the monetization models and technological development opportunities within the quantum computing industry?

At the first “Committee Member Channel” of the Fourth Session of the 14th National Committee of the Chinese People’s Political Consultative Conference on March 4, Pan Jianwei, Executive Vice President of the University of Science and Technology of China, introduced several breakthroughs in China’s quantum technology during the 14th Five-Year Plan period. “We are vigorously advancing the development of quantum technology, with quantum communication maintaining international leadership, quantum computing firmly in the top tier globally, and multiple directions in quantum precision measurement making significant progress.” He stated, “During the 15th Five-Year Plan, we will continue to strengthen original innovation, promote deep integration of industry, academia, and research, accelerate成果转化, and better serve the cultivation of new productive forces and high-quality economic and social development.”

In February 2026, IBM explicitly announced its quantum computing timeline at the Barclays “Quantum Unlock 1.0” investor event: achieving “quantum advantage” in 2026 and fault-tolerant computing by 2029. This roadmap provides the most practical technical milestones so far, signifying that quantum computing is accelerating from laboratory validation toward industrialization.

The quantum computing industry has entered a period of “technological breakthroughs combined with commercial validation.” On one hand, superconducting technology, benefiting from semiconductor process compatibility and fast gate operations, has become the dominant approach for universal quantum computing, with engineering challenges replacing physical bottlenecks as the core obstacle to scaling; on the other hand, the migration to post-quantum cryptography (PQC) is urgent, with the threat of “pre-emptive acquisition and later decryption” pushing key sectors to accelerate deployment.

Based on an in-depth analysis of the industry chain, we have constructed a four-dimensional investment analysis framework: “Technology Roadmap - Industry Value - Timeline - Target Selection.” The core conclusions are as follows: upstream core equipment such as dilution refrigerators and measurement/control systems are benefiting from domestic substitution and are expected to deliver early performance; quantum cloud platforms and PQC security are likely to become mid-term monetization anchors; while complete machines still await the true turning point in the fault-tolerant era around 2029.

Studying the quantum industry first requires understanding its fundamental differences from classical computing.

① Technology Roadmap Dimension: Superconducting route dominates, multiple paths compete

IBM chooses superconducting qubits as its core technology route, based on three reasons:

Quality: single-qubit error rates have improved from 10⁻¹ to 10⁻⁴ over six years, a significant enhancement

Scalability: superconducting qubits can be manufactured using mature lithography processes, highly compatible with existing semiconductor production lines

Speed: gate operation speeds are thousands of times faster than ion traps and neutral atoms

The compatibility with semiconductor manufacturing and decades of microwave engineering experience give superconducting qubits a structural advantage in practical universal quantum computers.

Although superconducting technology leads, other approaches still have advantages in specific scenarios:

Photonic quantum: long coherence times, compatible with fiber-optic communication; “Jiuzhang 3” has achieved 255-photon quantum supremacy

Ion traps: long coherence, high control precision; IonQ’s #AQ 64 performance is leading

Neutral atoms: naturally uniform qubits, scalable arrays; QuEra has developed a 256-atom system

Silicon spin: compatible with CMOS processes, small footprint; Intel’s Tunnel Falls has shipped products

Understanding quantum computing requires grasping the industry reality of “multiple paths”—different technical approaches excel in core metrics like qubit count, fidelity, and coherence time, and are unlikely to be interchangeable in the short term.

② Industry value dimension: Upstream and midstream dominate, growth prioritized

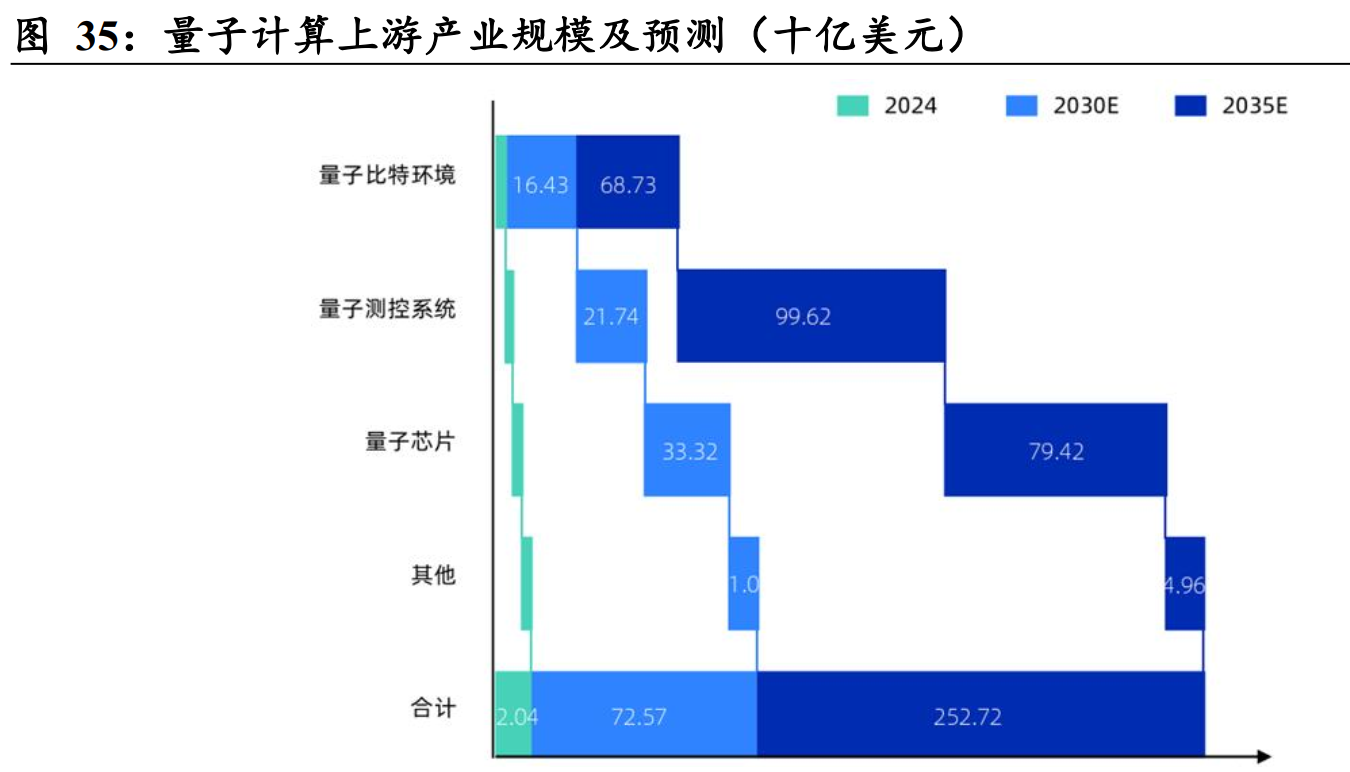

The quantum industry chain shows a clear “upstream and midstream dominance” feature. According to photon box data, in 2024, the global quantum computing market structure is approximately 40% upstream, 46% midstream, and only 14% downstream. Upstream focuses on core hardware like dilution refrigerators, measurement/control systems, and quantum chips; midstream covers prototypes and complete systems; downstream involves quantum cloud platforms and vertical applications.

Because upstream and midstream segments have clear technical barriers and hardware needs, and under the context of自主可控 and国产替代, they are more likely to secure orders and revenue upfront, becoming the market’s primary growth tracks. The upstream market size is expected to explode from $2.024 billion in 2024 to $72.57 billion in 2030, with a CAGR of 78.3%.

③ Timeline dimension: IBM’s roadmap provides clear coordinates

IBM’s “Practical Stage → Quantum Advantage → Fault Tolerance” three-phase roadmap offers a clear industry evolution timeline:

The significance of this timeline lies in shifting quantum computing investment from “hype” to a “milestone validation” rational framework. Investors can monitor the realization of key milestones and adjust their strategies dynamically.

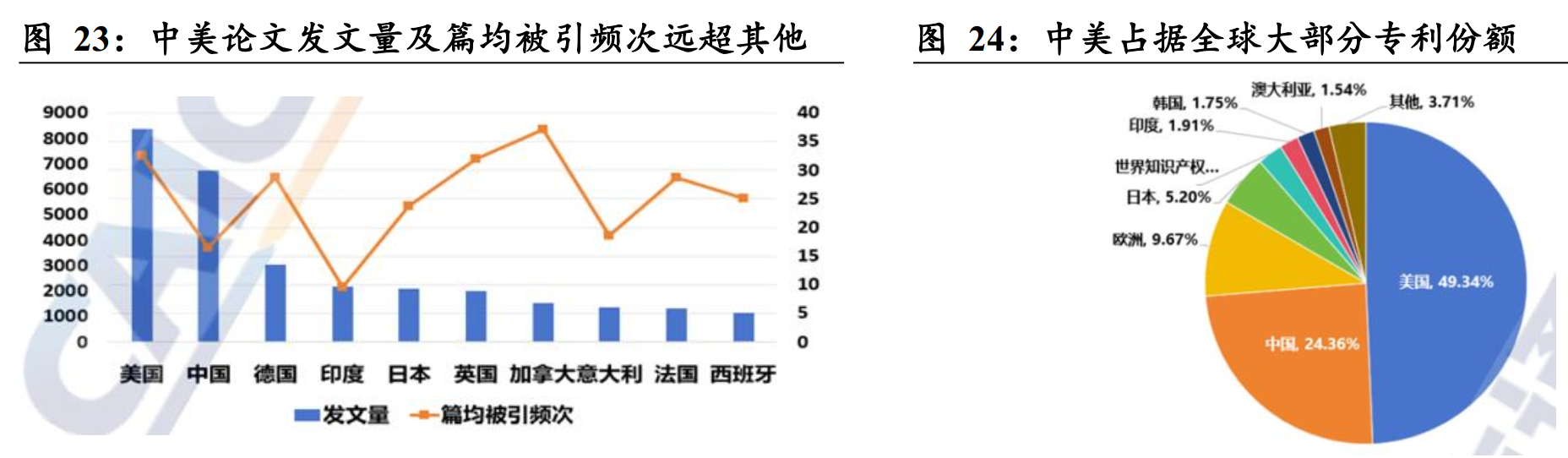

④ Competitive landscape: US and China lead, domestic gap narrowing

Globally, the US and China dominate the first tier. The US leads in the number of quantum companies (215), investment activity (50% of global funding), and ecosystem completeness; China follows with 145 companies and 107 in number, leading in quantum communication, with quantum computing complete machines reaching international levels.

Domestically, prototypes like “Zuchongzhi 3” and “Ben Yuan Wukong” have achieved core parameter benchmarks comparable to international standards, with intergenerational gaps narrowing both domestically and abroad. However, in critical segments like dilution refrigerators and high-end measurement/control equipment, there remains an urgent need for国产替代 driven by export controls from Western countries.

Based on the above framework, we have developed a “Technology Route × Industry Value × Timeline × Safety Margin” four-dimensional investment screening model:

① Dimension One: Technology Route—Focus on superconducting mainline, consider特色路径

The core strategy is to hold a main position in the superconducting route, with satellite positions in photonic and ion trap approaches. Key targets include IBM, Google, GuoDun Quantum, and Ben Yuan Quantum. The superconducting route benefits from semiconductor process compatibility, with the clearest path to industrialization, suitable for long-term allocation.

② Dimension Two: Industry Value—Prioritize upstream core equipment

The main strategy is to prioritize allocations in dilution refrigerators, measurement/control systems, and other upstream core hardware, which have the “rigid demand + high barriers +国产替代” logic.

Dilution refrigerators: In 2024, the global market is about $283 million; domestic vendors have broken through 10mK-level technology. Focus on Hesin Instruments (quantum裁技术), GuoDun Quantum (ez-Q Fridge), Ben Yuan Quantum (Ben Yuan SL series).

Measurement/control systems: Market could reach $21.74 billion by 2030. Focus on GuoDun Quantum (ez-Q Engine 2.0), Zhongwei Daxin (QCS1000), Ben Yuan Quantum (Ben Yuan Tianji).

Quantum chips: CAGR expected at 62.3% from 2024-2035. Focus on GuoDun Quantum (504-bit “Xiaohong”), Ben Yuan Quantum (72-bit “Wukong芯”), GuoYi Quantum (NV center sensors).

③ Dimension Three: Timeline—Grasp three key windows

Window 1 (2026): Realization of quantum advantage. Monitor supply chains related to Nighthawk processors and domestic superconducting quantum computer orders. GuoDun Quantum and Ben Yuan Quantum are expected to benefit first.

Window 2 (2027-2028): Scaling of quantum-classical hybrid computing. Track growth in quantum cloud platform users and commercialization progress. Platforms like China Telecom “Tianyuan,” Ben Yuan Quantum Cloud, and Quansheng Technology are worth following.

Window 3 (2029): Fault-tolerance inflection point. Focus on pre-application explosive opportunities, including PQC security, materials simulation software, and financial optimization algorithms.

④ Dimension Four: Safety Margin—Find certainty in “Quantum+” paths

The core strategy is to identify certain monetization paths for “Quantum+”—including:

Post-quantum cryptography: The threat of quantum computing to current cryptosystems is certain; PQC migration is imperative. Focus on companies like Geer Software, Sanwei Xin’an, and Xin’an Century.

Quantum-classical hybrid computing: IBM and AMD have validated the tightly coupled trend of “classical computing power + quantum computing power,” creating incremental demand for CPUs and GPUs.

Quantum precision measurement: GuoYi Quantum has broken foreign monopoly in electron paramagnetic resonance spectroscopy, with a 25% global market share, offering certain国产替代空间.

Conclusion: Quantum computing is moving from a technological singularity toward industry validation~

IBM’s quantum timeline provides clear industry evolution coordinates. Investment in quantum computing is shifting from “hype” to a rational “milestone validation” phase. Over the past decade, quantum computing has been viewed as “future technology.” However, the market environment fundamentally changed in 2026. Quantum computing is not a replacement for classical computing but a complement.

For investors interested in the quantum industry, a “dumbbell strategy” is recommended: one end embracing tech giants like IBM and Google with deep moat; the other end focusing on specialized and innovative enterprises making国产替代 in key upstream segments like dilution refrigerators and measurement/control systems.

Risk Warning and Disclaimer

Market risks exist; investments should be cautious. This article does not constitute personal investment advice and does not consider individual users’ specific investment goals, financial situations, or needs. Users should evaluate whether any opinions, views, or conclusions herein are suitable for their circumstances. Invest accordingly at their own risk.